Stop Lifestyle Creep: Master Wealth Psychology & Grow Savings

Understanding Lifestyle Inflation: The Hidden Threat to Wealth

In an era where personal incomes are frequently rising, a peculiar paradox often emerges: despite earning more, many individuals find themselves under persistent financial strain. This phenomenon, widely recognized as lifestyle inflation or lifestyle creep, refers to the gradual increase in discretionary spending that escalates in direct correlation with an individual’s rising income. Recent financial analyses highlight that while U.S. consumer spending saw a nearly 6% increase across all income demographics between 2022 and 2023, a concerning minority—only 54% of adults—possessed adequate savings to cover three months of essential expenses. This data starkly illustrates a critical trend: as earnings ascend, the propensity for expenditures to rise concomitantly leaves little room for substantial saving or wealth accumulation.

Lifestyle inflation is not inherently detrimental. Indeed, an augmented income should logically translate into an enhanced quality of life. However, without judicious management and predefined financial boundaries, these incremental upgrades—ranging from more expensive dining experiences to larger residential properties or premium subscription services—can subtly but profoundly undermine the long-term financial security one strives to cultivate. A comprehensive understanding of the psychological underpinnings of this behavioral tendency is thus paramount for effective financial mastery.

The Psychology Behind Escalating Expenditures

The inclination to increase spending in tandem with rising income is often more of a subconscious psychological reaction than a deliberate financial choice. Behavioral economists frequently attribute this pattern to hedonic adaptation—a fundamental human predisposition to rapidly acclimatize to novel comforts and elevated living standards. This adaptation subsequently necessitates a continuous pursuit of further upgrades to sustain the initial level of satisfaction or perceived well-being.

Consider, for instance, the experience of a luxury hotel stay. The initial encounter might evoke a profound sense of novelty and specialness; however, with repeated exposure, such experiences quickly become normalized. This identical pattern manifests in routine consumer behaviors involving vehicles, apparel, technological devices, and even housing. Furthermore, psychologists underscore the considerable influence of social comparison. As peers showcase their lifestyle enhancements on various social media platforms, individuals often experience an unconscious pressure to maintain parity or "keep up," fueling further discretionary spending.

Pioneering research by scholars like Richard Thaler and Cass Sunstein, authors of the seminal work Nudge, indicates that these cognitive biases are not merely indicative of personal weakness but rather intrinsic aspects of human neurological wiring. Humans are naturally programmed to adapt and benchmark their status against others. Consequently, the challenge extends beyond simply resisting immediate temptations; it involves strategically re-engineering one's financial ecosystem to facilitate automatic savings and investment behaviors.

Statistical Insights into American Spending Habits

Contemporary data from authoritative sources such as the Bureau of Economic Analysis (BEA) and the Federal Reserve reveal a dramatic decline in U.S. personal saving rates since their peak during the 2020 pandemic. By mid-2025, these rates hovered around a meager 4%, a stark contrast to the over 20% observed amidst lockdown periods. Concurrently, various sectors, notably technology, healthcare, and finance, have witnessed appreciable increases in real wages.

Despite these wage gains, approximately one-third of Americans continue to operate on a paycheck-to-paycheck basis, a phenomenon that extends even to households earning in excess of $100,000 annually, as reported by Bankrate. Early 2025 data also indicated a troubling surge in credit card debt, surpassing an unprecedented $1.1 trillion nationally. These aggregated statistics unequivocally demonstrate that elevated earnings frequently culminate in augmented spending rather than a tangible enhancement in financial stability or long-term security.

Differentiating Intentional Upgrades from Financial Drift

It is crucial to distinguish between a conscious, value-aligned lifestyle improvement and unchecked financial drift. If, after years of diligent effort, one is able to afford a more comfortable home, superior healthcare provisions, or enriching experiences that genuinely enhance overall well-being, such expenditures represent prudent allocations of resources. The essence of sound financial management lies in striking a delicate balance: prioritizing intentional enhancement over automatic expansion.

To conceptualize this distinction, consider purposeful life upgrades as indicators of financial progress, whereas habitual spending increases signify financial drift. An analysis by Investopedia in 2025 underscored that the primary issue arises when seemingly innocuous indulgences—such as daily premium coffee, multiple streaming service subscriptions, or frequent technology upgrades—cumulatively transform into significant financial drains. Over extended periods, these "invisible upgrades" can siphon thousands of dollars annually, funds that could otherwise be strategically deployed for substantial growth through compounding investments.

The Compounding Cost of Lifestyle Creep

The true financial burden of lifestyle creep is perhaps best understood through the lens of "compounding in reverse." Illustratively, consider a 30-year-old individual who receives a $10,000 salary increment. Should they judiciously allocate half of this raise, equating to $5,000 per year, into a 401(k) account yielding an average annual return of 7%, they could potentially amass over $500,000 by the age of 60. Conversely, if the identical $5,000 is diverted towards new consumption patterns—such as vehicle leases, novel gadgets, or increased restaurant dining—it is effectively expended, offering no future financial return.

The divergence here is not merely arithmetical but profoundly psychological. Individuals frequently rationalize increased spending as well-deserved rewards, yet seldom undertake the critical exercise of calculating the immense future value that money could have attained through investment. As one seasoned financial planner aptly articulates, "Every dollar you don't invest today is a future version of yourself that has fewer choices," emphasizing the profound long-term implications of immediate gratification.

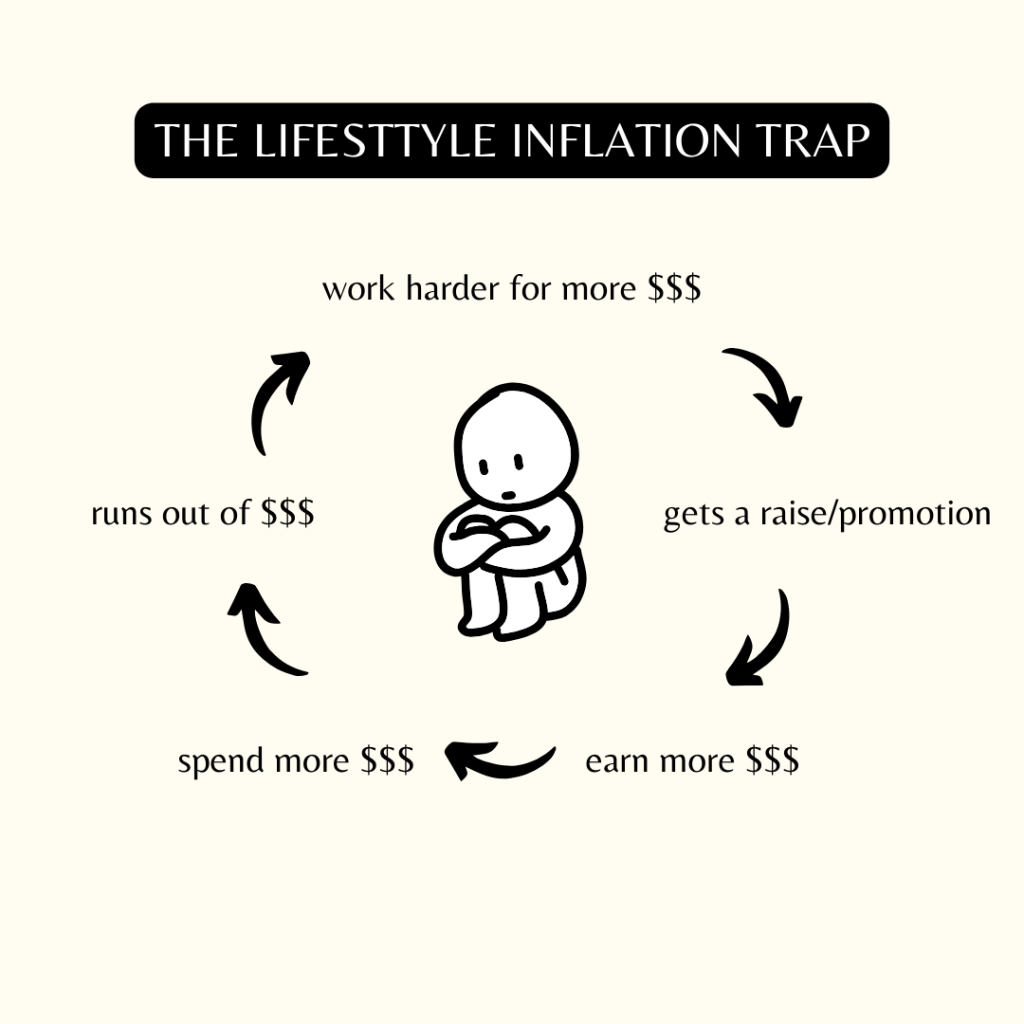

The image above visually encapsulates the "lifestyle inflation trap," where rising income without proportional savings leads to a cycle of increased spending and persistent financial stress, even for high earners.

Strategies to Counter Lifestyle Inflation

Mitigating the effects of lifestyle inflation does not necessitate an austere budget devoid of enjoyment. Rather, it involves meticulously aligning spending with one's core values and instituting clear structural mechanisms for managing salary raises, bonuses, and unexpected financial windfalls. The most financially astute individuals in 2025 are employing the following proactive strategies:

1. Prioritize Automated Savings

- Implement direct, automatic transfers to channel a predetermined portion of every salary increase directly into savings accounts or investment portfolios. This approach effectively treats savings as a non-negotiable financial obligation. Research from reputable institutions like Vanguard and the Consumer Financial Protection Bureau indicates that financial automation significantly boosts long-term savings rates, often by over 40%.

2. Establish a "Raise Rule"

- Before a salary increment is reflected in a paycheck, proactively decide on its allocation. A commonly advocated guideline is the 50-30-20 rule: dedicating 50% to strategic financial objectives (such as investments, debt accelerated repayment, or bolstering an emergency fund), 30% for carefully considered lifestyle enhancements, and the remaining 20% for taxes or establishing a buffer fund.

3. Analyze Emotional Spending Triggers

- Diligently identify the underlying emotional drivers of increased spending, which may include stress, social comparison, boredom, or the desire to affirm professional success. Engaging in introspective practices, such as journaling or meticulously tracking the motivations behind significant purchases, can unveil recurring patterns, thereby enabling more deliberate and controlled spending decisions.

4. Define Your Financial Comfort Zone

- Lifestyle creep frequently occurs when individuals fail to articulate a precise definition of "enough." It is prudent to predefine what constitutes a "comfortable" standard of living across various domains—including housing, transportation, and leisure activities—to prevent an endless escalation of material expectations.

5. Build Robust Safety Nets

- Before indulging in any form of luxury upgrade, prioritize the establishment of a robust financial safety net. A 2024 Bankrate survey revealed that only 44% of Americans possess the capacity to cover an unforeseen $1,000 expense without resorting to borrowing. Ensuring that an emergency fund adequately covers at least three to six months of living expenses is a fundamental prerequisite for genuine financial security.

Conclusion: The True Value of Financial Awareness

Lifestyle inflation predominantly thrives in an environment of financial autopilot. The crucial moment one begins to consciously scrutinize the destination of their supplementary income marks the initial, decisive step toward regaining control. The contemporary landscape reveals that Americans, while often earning more, are paradoxically saving less—a testament to the fact that the delineation between financial instability and robust financial freedom is not merely a function of income, but profoundly a matter of intentionality.

By meticulously setting clear financial objectives, automating saving mechanisms, and ensuring that every perceived upgrade is a conscious and justifiable choice, individuals can effectively transform money from a fleeting resource into a powerful tool that actively works in their favor. True wealth, in its most profound sense, is not characterized by increased expenditure but by the invaluable acquisition of greater time, enhanced security, and profound peace of mind.